Calculate Monthly Savings with our Auto Loan Refinance Calculator

Data updated: April, 2026

Refinance Calculator

Adjust the sliders to model your new loan terms.

🔒 No data stored, calculations run entirely in your browser 📊 Standard amortization formula, results match your loan contract

🏦 Independent tool, no lender affiliations or referral fees ✅ No sign-up required 🔄 Rates reviewed monthly by Marcus J. Holloway

How to use the Auto Loan Refinance Calculator

Enter your current loan details. If you aren’t sure of your 10-day payoff amount, your latest monthly statement will have the closest estimate.

Real-World Scenarios

The effectiveness of an auto loan refinance calculator depends on your vehicle type and current loan-to-value (LTV) ratio. Here is what we are seeing in the current market:

- The Tesla Opportunity: 2024 Model Y owners who financed at 12% are successfully moving to 5.8% APRs this month.

- The Truck Strategy: For heavy-duty models like the Silverado or F-150, a 3.5% rate drop can eliminate over $12,000 in interest over the life of the loan.

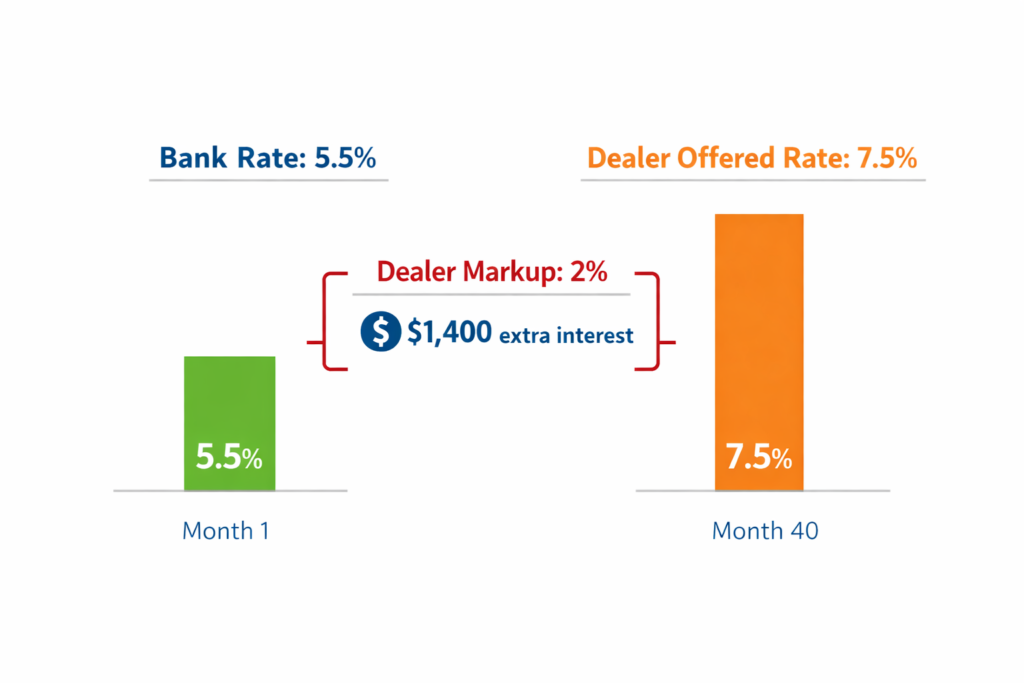

Why Drivers are Moving Away from Captive Financing

If you originally financed your vehicle through a “Captive” lender (like the dealership’s own bank), you likely paid a “convenience premium”. Modern 2026 data shows a massive shift toward credit union refinancing for better rates.

- The Disconnect: Dealerships rarely disclose that an auto loan refinance calculator can reveal a “hidden” 2% to 4% APR saving simply by switching lender types.

- Targeted Savings: This is especially relevant for owners of high-value trucks and electric vehicles who were funneled into restrictive introductory contracts.

Refinancing with Negative Equity

If our auto loan refinance calculator shows a potential rate drop, but your loan balance is higher than your car’s current value, you aren’t necessarily stuck. In the current market, many credit unions allow for 125% Loan-to-Value (LTV) refinancing.

- The Move: If you owe $30,000 on a car worth $25,000, you have $5,000 in negative equity.

- The Strategy: Instead of a standard refi, look for “LTV-Friendly” lenders. Dropping your rate while keeping your term short can help you reach “equity break-even” months sooner than staying with a high-interest dealer loan.

Dealer Financing vs. Refinancing Through a Bank or Credit Union

Most car buyers finance at the dealership because it is easy. The dealer handles the paperwork, the loan funds at the same time as the car purchase, and you drive home the same day. The trade-off is that dealer rates are almost always higher than what you would get by applying directly.

Here is a practical comparison for a $28,000 loan over 60 months:

| Dealer Financing | Direct Lender Refinance | |

| Typical APR (good credit) | 7.5% to 9.0% | 5.0% to 6.5% |

| Monthly payment (on $28k/60mo) | $562 at 8% | $540 at 6% |

| Total interest paid | $5,734 | $3,679 |

| Difference | $2,055 saved | |

| Time to apply | Same day at dealership | 3 to 7 days online |

| Rate shopping possible? | Limited at point of sale | Yes, multiple lenders |

Credit unions tend to offer the most competitive refinance rates for borrowers with good credit. They are non-profit institutions, which generally means lower rates than traditional banks. Many allow you to join specifically to access their auto loan products.

Online lenders have expanded refinance availability significantly. Most offer pre-qualification with a soft credit check, meaning you can see your rate estimate before committing to a hard inquiry. Shopping 3 to 5 lenders within a 14-day window is treated as a single inquiry by most credit scoring models.

Current Auto Loan Refinance Rate Benchmarks

Last reviewed: 2026 by Marcus J. Holloway

Lenders price auto refinance rates based primarily on credit score tier. The ranges below reflect current averages across major banks, credit unions, and online lenders. Individual offers will vary based on loan term, vehicle age, and LTV ratio.

| Credit Tier | Score Range | Typical Refinance APR |

|---|---|---|

| Super Prime | 781 and above | 4.5% to 5.5% |

| Prime | 661 to 780 | 5.5% to 7.5% |

| Near Prime | 601 to 660 | 7.5% to 11.0% |

| Subprime | 501 to 600 | 11.0% to 16.0% |

| Deep Subprime | 500 and below | 16.0% to 22.0%+ |

Rate ranges are updated periodically. For the most current offers, use pre-qualification tools from at least 3 lenders before applying.

The “Self-Insured” Strategy for 2026

A lower monthly payment on your auto loan refinance calculator is only half the battle. Since car insurance and repair costs remain elevated, you need to protect your savings.

- The 50/50 Rule: When you save $100 a month through refinancing, consider reallocating $50 into a dedicated vehicle repair fund.

- Why It Matters: This creates a buffer against the high-cost tech repairs common in modern vehicles, ensuring your refinancing success isn’t wiped out by a single mechanical failure.

What the Savings Look Like in Practice

Here is a before-and-after for a typical refinance scenario. The borrower originally financed at a dealership and is now 8 months into the loan.

| Current Loan | After Refinancing | |

| Remaining balance | $21,400 | $21,400 |

| APR | 9.5% | 5.8% |

| Months remaining | 52 | 52 |

| Monthly payment | $480 | $452 |

| Monthly savings | $28 per month | |

| Total interest remaining | $3,540 | $2,058 |

| Total interest saved | $1,482 | |

| Refinance fees | $200 | |

| Breakeven point | 8 months | |

| Net savings (keep 3 yrs) | $1,282 |

The $28 monthly saving looks small on its own. But across 52 months it adds up to $1,482 in interest. After the $200 fee, the net gain is $1,282 for about 20 minutes of paperwork. The breakeven is month 8, meaning if the borrower keeps the car for at least 8 more months, they come out ahead.

Enter your own numbers at the top of this page to see your specific result.

Compare your current rate against those benchmarks to see where you stand.

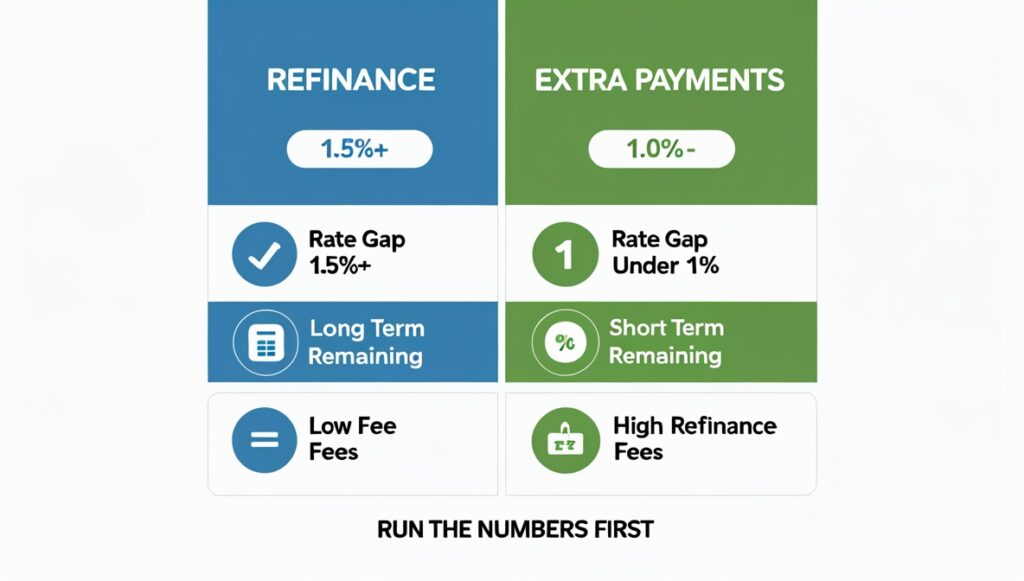

When Extra Payments Beat Refinancing

Refinancing makes sense when the rate improvement is large enough to justify the fees and the paperwork. But there is a situation where skipping the refinance and simply making extra principal payments produces a better outcome: when your rate gap is small and your remaining term is short.

If your current rate is 6.5% and the best available refinance rate is 5.8%, the gap is 0.7 points. On a $12,000 balance with 24 months remaining, that saves about $84 in total interest, before fees. If refinance fees run $200 to $300, you come out behind.

In that scenario, putting the same $200 directly toward principal reduces your balance immediately and cuts interest on every remaining payment without any paperwork, hard inquiry, or title transfer. Use the auto loan refinance calculator to compare both options with your actual numbers before deciding.

Video Walkthrough

Avoiding the Refinance

Short, practical rules to protect your wallet.

The Term-Extension Trap

Lowering your payment by adding months can increase total interest. If you extend a 36-month balance to 60 months, you pay interest for two extra years. Always compare the total interest paid, not just the monthly number.

Negative Equity

High LTV is the top reason for denial. If you owe more than the car is worth, consider a cash-in payment or wait until you pay down the balance. Rolling negative equity into a new loan raises your financed amount and the interest you pay.

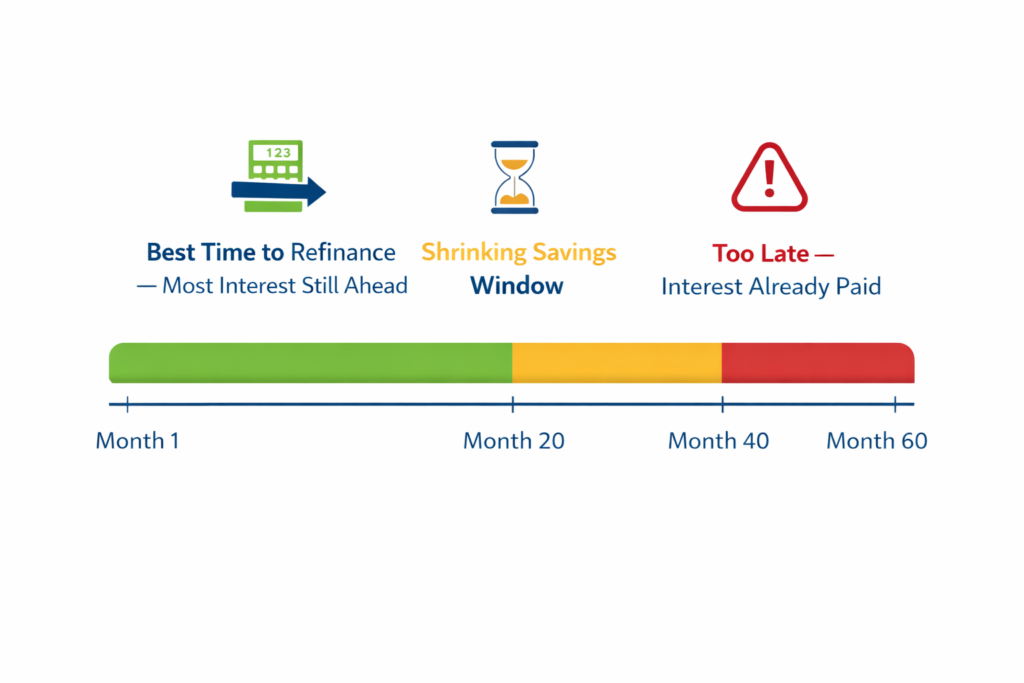

The 10-Day Payoff Requirement

A current balance is not the final payoff amount. For 100% accuracy in savings projections, utilize the figure from a formal 10-day payoff statement, which accounts for daily interest accrual since your last payment.

Our Methodology

We use the standard fixed-rate amortization formula so results match your loan contract.

FAQs

Q: Does refinancing hurt my credit score?

A: A soft pre-qualification does not impact your score. However, a final application involves a hard credit pull, which typically causes a small, temporary dip in your credit profile.

Q: What is the “1% Rule” for refinancing?

A: A common financial benchmark is to refinance only if you can reduce your APR by at least 1.0% to 1.5%. This ensures the interest savings outweigh the costs of the transaction.

Q: Does a lower APR mean it’s a better deal and we should take it?

A: A lower APR doesn’t always mean a better deal. You must account for administrative fees, title transfer costs, and early payoff penalties. The Auto Loan Refinance Calculator factors these into your Breakeven Analysis. If it takes 14 months to “break even” on the fees, but you plan to sell the car in 12 months, the refinance is mathematically unsound.

Q: When should I use an auto loan refinance calculator?

A: You should run your numbers if your credit score has improved by 40 points or if you haven’t checked market rates in the last six months.

Q: What is the “2% Rule” in 2026?

A: If the auto loan refinance calculator indicates a rate drop of 2% or more, the administrative benefits usually outweigh the processing time within 90 days.

About the Developer: I am a technical specialist focused on building transparent financial tools. This auto loan refinance calculator was developed to provide an ad-free, data-first alternative to bank-owned lead generators. I update the calculation logic monthly to ensure it matches 2026 federal lending standards.

Ready to test your specific numbers? Enter your loan details in the Auto Loan Refinance Calculator at the top of the page and get a downloadable amortization table.